.jpg)

Side Letters

Side Letters is a collection of essays, research, and analysis on how investment firms communicate with investors, management teams, and transaction partners. The focus is practical: how firms articulate value, build credibility, and navigate increasingly complex evaluation environments.

Featured Videos

Most emerging managers believe they have a narrative because they can describe their strategy. But narrative is not description. Narrative is structure — the sequence, logic, and emotional progression that allows an LP to understand why a category matters, why a particular angle makes sense, and why this manager might be worth backing. A pitchbook is the first time an emerging manager is forced to express that structure outside of conversation, without the ability to clarify, expand, or recalibrate in real time. It exposes whether the story has bones or whether it’s being held together by enthusiasm and improvisation. And for Fund I and Fund II managers, narrative structure is often the difference between a deck that feels like the beginning of a real institutional story and one that feels like a loose collection of ideas.

1. A Strong Fund I Narrative Begins With Category, Not Credentials

Emerging managers frequently begin their pitchbooks by describing themselves: bios, backgrounds, decades of combined experience. But LPs don’t have the frame yet. They don’t know what the team is applying that experience to. Narrative structure starts one level higher — with the category. What is the space you operate in, and why is it worth anyone’s attention? In an early-stage deck, the category is not assumed; it has to be established cleanly. If LPs don’t understand the world you’re investing in, they won’t know how to interpret anything that follows. The category sets the altitude. And in Fund I fundraising, altitude determines whether the rest of the narrative ever lands.

2. The Strategy Must Feel Like the Natural Response to That Category

Once the category has been framed, the strategy has to emerge as the logical next step — not as a standalone set of tactics. LPs want to feel a sense of inevitability: given the structure of this market, here is the approach that makes the most sense. This is where emerging managers often lose momentum. They describe a strategy with plenty of detail but very little connective tissue. There’s no narrative bridge from “here’s the opportunity” to “here’s the right way to pursue it.” Good narrative structure makes the strategy feel like the only sensible response to the category you just described, not one of many plausible approaches floating in conceptual space.

3. Sequencing Is a Psychological Tool, Not a Formatting Choice

The order of slides is not an aesthetic decision; it’s a cognitive decision. When you open a deck with a track record — even a good one — the LP has no idea what that track record means yet. They lack context: track record for what? Similarly, when you lead with a process diagram, the LP doesn’t know why the process matters. They haven’t been taught the dynamics of the market or the underlying thesis. This is why the executive summary belongs first, then the category, then the strategy, then (and only then) the credentialization. Emerging managers who get sequencing right create narrative momentum; those who get it wrong force the LP to hold disconnected ideas in their mind and assemble the story themselves. LPs rarely choose to do that work.

4. Effective Pitchbooks Use Examples to Make the Strategy Tangible, Not Decorative

Emerging managers often struggle with how to incorporate examples — prior deals, pre-fund deals, warehoused assets, or selected historical experience from earlier firms. The instinct is to throw the examples into the middle of the deck or to use them as early-stage “proof.” But examples are not proof; they are narrative illustration. Their job is to show what the strategy looks like in the real world and to give texture to the thesis. When examples appear too early, they feel orphaned from the story; when they appear too late, they feel like an afterthought. When examples appear right after the strategy section, they reinforce the thesis and make the story concrete. LPs stop seeing a theoretical angle and start seeing an investable one. That shift — from abstract to tangible — is where narrative structure begins to create memory.

5. Narrative Structure Lives or Dies in the First Five Slides

Every emerging manager believes LPs will “get to” the important part. LPs don’t get to anything. They skim, they flip, and they decide whether the story is worth tracking. The first five slides are the narrative’s opening scene. If the opening doesn’t establish the category, the angle, and the promise of the story, the LP rarely reads far enough to see the nuance. Think of it as the pilot episode of a television series: you don’t get eight hours to win someone over. You get 40 minutes. Emerging managers who bury the thesis halfway through the deck are essentially asking LPs to wait until episode eight before it gets good. Nobody does that anymore.

Closing Thought

Narrative structure is what makes a pitchbook coherent, memorable, and emotionally legible. Emerging managers often mistake narrative for polish. But LPs don’t respond to polish; they respond to clarity. They want a story that makes sense on its own terms, that emerges in the right order, and that gives them enough structure to evaluate the idea without doing interpretive work. The pitchbooks that succeed aren’t the ones with the best diagrams or the most slides. They’re the ones that teach the LP how to think about a category, an angle, and a team — in a way that feels unmistakably intentional.

Emerging managers don’t fundamentally misunderstand pitchbooks. Most of the people who make it to Fund I are rational, competent, and thoughtful. The problem isn’t intelligence; it’s framing. They’re building decks as if LPs were primarily evaluating the information, when in reality LPs are evaluating the story around the information — and, more specifically, whether that story feels investable for a first- or second-time fund.

From an LP’s perspective, a Fund I or Fund II pitchbook isn’t an encyclopedia. It’s a test. It answers three questions very quickly:

- Is this a real firm or a concept in motion?

- Is there a coherent way to think about this strategy?

- Is there anything here I’ll remember tomorrow?

Most early decks fail one of those tests, and usually for avoidable reasons.

LPs Don’t Want a Miniature Version of a Fund VII Deck

One of the most common mistakes I see is spinouts copying their former employer’s materials. A manager leaves a large platform, takes the Fund VII deck as a mental template, and tries to shrink it into a Fund I format. It doesn’t work.

Fund VII decks are designed to situate a new vehicle inside a 20–30 year arc:

here’s where we’ve been, here’s how we’ve performed, here’s how the strategy has evolved, here’s what’s different this time. LPs reading those decks already know the franchise. They need context.

Fund I decks have the opposite job. There is no arc. There is no franchise history. The LP isn’t asking “how has this strategy evolved?” They’re asking “what exactly is this, and why should I care?”

Those are radically different questions. Using a Fund VII blueprint for a Fund I pitchbook is like using a retirement speech outline as a template for a debut.

The First Five Slides Are the Real Deck

LPs don’t read pitchbooks linearly the way managers imagine. They skim, they flip, they pause, they decide whether to keep going. In that sense, the first five slides are the deck. Everything that comes after is optional.

What LPs need out of those opening slides is simple:

- a clear explanation of the category,

- an understandable angle,

- and a sense that the manager knows exactly what they’re trying to build.

Too many emerging managers use their early slides for a deal funnel graphic, an investment process diagram, or a collage of buzzwords. No one has ever become excited about a new manager because they saw a diagram showing “proprietary deal flow” and an arrow labeled “value creation.”

If a reader doesn’t understand what you are, where you play, and why your angle is interesting within five slides, they usually don’t keep going. It’s like a new TV show: if the first episode doesn’t land, no one is waiting until episode eight for it to “get really good.”

LPs Want Category Education and Ownership of the Angle

For Fund I and II, the pitchbook is not primarily persuasion. It’s category education plus ownership of the angle.

You’re not trying to prove that you’re “better than” the usual suspects. You’re trying to:

- convince the LP that this slice of the world is worth allocating to, and

- convince them that you are the sharpest expression of that slice.

That’s a different mindset than the benchmark-heavy, context-heavy approach in a later-fund deck. LPs reviewing emerging managers are usually asking, “Do I believe this corner of the market deserves attention? And if I do, is this the right team to explore it?”

The deck has to make that pair of arguments cleanly.

Track Record Is Secondary to Strategy — Especially When You Can’t Own It

LPs don’t expect a pristine track record from a first-time fund. They do expect honesty and proportion.

Spinouts from larger firms are usually constrained: they can’t port formal attribution, they can’t present full performance histories as “theirs,” and they can’t pretend the prior platform didn’t matter. LPs know this. They’ve seen it a hundred times.

What LPs want in that scenario is not a tortured attempt to make the past do more work than it can. They want a crisp strategy and a handful of real examples that show how the manager thinks. The past is useful context — but only when it reinforces the forward-looking story.

If you can’t own the track record, you shouldn’t let the pitchbook behave as if you can. Credentialize, yes. Over-credentialize, no. LPs are far more interested in whether your angle is coherent than whether you can stack logos on a page.

LPs Expect the Deck to Make the Blind Pool Less Blind

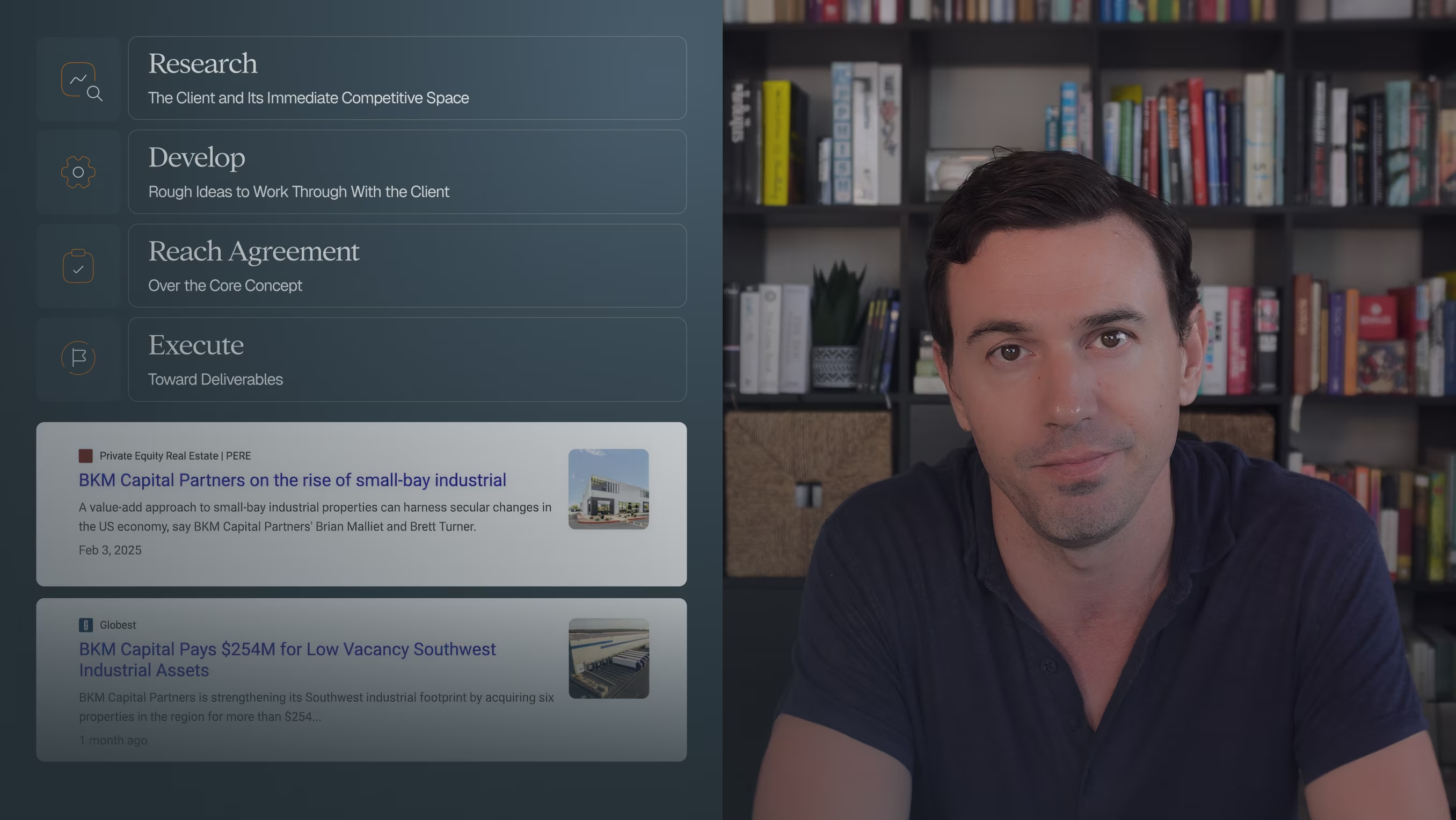

For managers who have done pre-fund or warehoused deals, the best Fund I decks use those deals to make the fund feel less hypothetical. BKM is a good example: six properties on balance sheet, financed by the founders, used not as “look how great we are” case studies, but as tangible evidence of what the fund will actually own.

LPs appreciate this not because they’re desperate for early marks, but because it gives them texture. It shows how the strategy behaves in the real world. The pitchbook stops being abstract. It becomes a guided tour of what the fund is likely to look like.

The same logic applies whether you’re doing real estate, private equity, credit, or some niche in between. Real deals make everything sharper — if they’re framed properly.

Closing Thought

LPs aren’t asking emerging managers for perfection. They’re asking for a few clear things: an understandable category, a believable angle, and a story that doesn’t sound like everyone else’s. The pitchbook is where those elements first come together — or fail to.

The biggest risk in a Fund I deck isn’t that you’ll use the wrong shade of blue or one too many charts. It’s that you will sound like yet another manager with a process, a funnel, and nothing memorable to say. LPs are not short on decks. They’re short on decks that feel like the first chapter of something they’ll be glad they backed in ten years.

Emerging managers tend to think of brand and design as a matter of taste — something that should look professional, aesthetically coherent, and aligned with the firm’s personality. LPs experience it differently. For them, brand and design are not an expression of style; they are a diagnostic. They offer clues about whether the GP is organized, disciplined, mature, and institutionally aware. Most emerging managers would never describe themselves as “inexperienced,” yet subtle design signals often convey precisely that impression.

The challenge is that LPs make these judgments unconsciously, and they make them early. Before you discuss the first deal example or outline the logic of your strategy, the LP has already formed a view about whether you are a serious institutional contender or an interesting emerging group still finding its footing. These judgments are not always fair, but they are remarkably consistent — and they shape everything that follows.

1. The Brand Reflects the Mind Behind It

One of the quiet truths in fundraising is that LPs project brand and design choices onto the investment process itself. A disorganized deck suggests disorganized underwriting. A cluttered website suggests cluttered thinking. An overdesigned visual system suggests a focus on performance rather than precision. No LP would articulate this directly, but years of pattern recognition have made them sensitive to the correlation between presentation quality and organizational maturity.

This is why emerging managers often underestimate the consequences of their design decisions. They assume LPs will look past the imperfections and “focus on the strategy.” LPs do the opposite. When the brand feels misaligned with the seriousness of institutional capital, they anchor on credibility gaps: Does the GP understand the level of professionalism expected? Will the firm mature fast enough to support a real fund? What else are they underestimating?

The brand is the first exposure LPs have to how you think. They use it to infer everything else.

2. Many Emerging Manager Brands Signal Something They Don’t Mean

In practice, emerging manager brands fall into a handful of avoidable traps:

The Developer Brand:

Website looks like it was built from a real estate developer’s template — busy, image-heavy, slogan-driven, and full of generic claims about “partnership” and “value creation.” LPs read this as lack of institutional awareness.

The Broker Brand:

Overly polished, promotional, and transactional in tone. LPs interpret this as an orientation toward deal-making rather than disciplined fund management.

The Startup Brand:

Trendy typography, clever taglines, or design choices more common in venture-backed tech than in institutional investment. LPs see this as misalignment with the culture of fiduciary responsibility.

The “Just a Logo and a PDF” Brand:

Spartan to a fault. An underpowered website paired with a pitchbook that feels like it was assembled for a bank lender, not an allocator. LPs read this as underdeveloped organizational maturity.

None of these signals are fatal, but they shape the LP’s cognitive frame before the GP speaks a single word.

3. Consistency Signals Maturity

Institutional investors expect consistency across brand touchpoints because it reflects operational discipline. A website that feels one way, a deck that feels another, and messaging that shifts depending on the audience signals instability. Emerging managers often dismiss this as a minor problem — something to “clean up later.” LPs don’t see it that way. They assume inconsistency in materials reflects inconsistency in underwriting, reporting, or strategy execution.

Brand consistency is not decorative; it is a proxy for organizational readiness. LPs don’t need you to be large, but they do need you to be coherent. A consistent brand signals the GP is capable of sustained, rigorous thought across multiple dimensions of the firm.

4. Design Maturity Does Not Mean Flash

Another mistake emerging managers make is assuming that a highly polished, visually dynamic brand will make them look more sophisticated. In reality, the opposite is often true. Institutional design maturity is quiet. It is subtle. It avoids unnecessary theatrics. LPs respond to restraint because it reflects seriousness of purpose — not a desire to impress.

The question LPs are evaluating is not “Does this look great?” but “Does this feel like the work of someone who knows what they’re doing?” When the visual system is too clever or too stylized, LPs read it as compensation. They assume the GP is trying to cover for something — usually a lack of track record or a strategy that has not been tightened enough.

The best emerging manager brands have a kind of intellectual modesty to them. They project confidence, not swagger.

5. LPs Default to “Risk Lens” When Evaluating Early-Stage Brands

Because emerging managers are inherently riskier than established platforms, LPs begin each interaction with an unspoken question: “Is this real?” Brand and design are the fastest way to answer that question, for better or worse.

When LPs see:

- a coherent narrative,

- a disciplined visual system,

- thoughtful materials, and

- mature design restraint,

they subconsciously shift into “evaluation mode” rather than “filtering mode.”

When they see:

- mismatched styles,

- inconsistent tone,

- decks that feel thrown together, or

- branding that feels aspirational rather than grounded,

they shift into “risk identification mode.”

These are not subtle distinctions. They meaningfully affect LP behavior.

Closing Thought

Brand and design are not the decoration around the strategy. They are part of the strategy’s credibility. Emerging managers misinterpret this not because they lack taste, but because they underestimate the extent to which LPs use presentation quality as a proxy for operational maturity. The visual system around a Fund I or Fund II strategy sends dozens of signals in seconds — about discipline, seriousness, category fluency, and whether the GP understands institutional expectations.

In a world where LPs filter quickly and remember little, the brand becomes the scaffolding that makes the rest of the story believable. It is not peripheral. It is foundational.

Investor communication in real estate used to follow a predictable pattern. Closed-end funds ran annual meetings or semi-annual update calls with institutional LPs. Non-traded REITs delivered periodic webinars and mailed highly structured update packets. Advisor-distributed products issued their required reporting and hosted occasional introductions. Family-office vehicles communicated however the family wanted to communicate.

Today, those lines are blurred.

Every vehicle type now operates under heightened expectations.

Institutions expect clarity and brevity.

Family offices expect candor.

Advisors expect digestibility.

High-net-worth investors expect reassurance.

And all of them expect the manager to communicate cleanly, confidently, and without overwhelming them.

Against this backdrop, the investor presentation — whether delivered live, via webinar, or as an asynchronous deck — is no longer a box-checking ritual. It’s a primary storytelling moment. It’s one of the few chances a manager has to shape how investors understand the portfolio, the strategy, and the environment in which both are operating.

The challenge is that most real estate teams approach these presentations the way they approach their day-to-day: with detail first and structure second. But investors don’t absorb information that way, especially across formats. The more cyclical, complex, and multi-audience the real estate world becomes, the more a presentation must be engineered — not just assembled.

1. Every Vehicle Has a Presentation Format, Even If It Doesn’t Call It an “AGM”

Closed-end funds hold annual or semi-annual meetings, and these feel familiar to most managers. But nearly every other structure has its own equivalent:

- Non-traded REITs run quarterly investor webinars.

- Interval funds publish and present NAV commentary.

- 1031/721 platforms provide deal-by-deal property updates.

- Advisor-distributed products hold virtual education sessions.

- Family-office partnerships request periodic portfolio deep dives.

- Open-end funds host rolling update calls as conditions change.

The names differ.

The audiences differ.

The regulatory wrappers differ.

But the core purpose is identical:

orient the investor, contextualize the portfolio, and reaffirm the competence of the platform.

Investors are not waiting for a performance surprise; they’re waiting for narrative clarity.

2. Most Managers Overestimate What Investors Want to Hear and Underestimate How They Process Information

Real estate teams tend to live deeply inside their own operational details. They know every acquisition, every lease-up, every disposition, every property-level story. They know the underwriting nuance and the debt structure and the submarket dynamics. When preparing investor materials, it’s tempting to bring all of that detail into the presentation.

But investors — regardless of sophistication — do not process detail until they understand the frame. A strong investor presentation provides that frame quickly.

The structure rarely changes:

- Where are we in the cycle?

A calm, specific, non-alarmist explanation of the market environment. - How does that environment intersect with our strategy?

The update is more compelling when the strategy feels responsive to conditions. - What do we want investors to understand about the portfolio right now?

Not everything — just the essentials that illuminate the story. - Where is the team focused next?

Investors want orientation, not prediction.

Only after those pieces are established does property-level or segment-level detail become meaningful. Without that frame, the presentation becomes a tour of unrelated slides rather than a coherent briefing.

3. Webinars Are Their Own Medium — and They Expose Weakness Quickly

Many real estate managers deliver their most important presentations via webinar, especially in the REIT, interval, and wealth-channel segments. But webinars are unforgiving. Attention drops faster. Visual clutter becomes more noticeable. Dense slides feel heavier. The presenter’s pacing has an outsized effect on comprehension.

The constraints make clarity non-negotiable.

Slides must be cleaner.

Narratives must be tighter.

Photography must serve a purpose.

Exhibits must be readable on a laptop screen.

And the story must unfold in a sequence that feels almost inevitable.

A good webinar slide is not a meeting slide.

A good webinar slide is simpler, sharper, and more deliberate.

Done well, webinars can deepen connection with audiences who may never meet the manager in person. Done poorly, they highlight every weakness in the deck — and often every weakness in the presenter’s preparation.

4. Advisor and RIA Audiences Require a Different Sensibility

The advisor and wealth channels bring their own dynamics. Advisors are intermediaries; they must digest your story and pass it along. They cannot do that if the materials are too dense or too technical. They must be able to explain what the vehicle does in one or two sentences. They must be able to answer their clients’ surface-level questions without returning to the manager every time.

This means investor presentations for advisor-distributed products cannot simply be simplified versions of institutional decks. They require their own design logic:

- fewer slides,

- fewer exhibits,

- clearer language,

- more narrative support,

- direct framing of “what this means for investors,”

- and visuals that can scale down into 4-pagers, landing pages, or email follow-ups.

Many managers underestimate how much of their capital formation success — or failure — comes down to whether advisors feel equipped to retell the story.

5. Consistency Across Presentations Builds Credibility Over Time

Whether the format is a webinar, a live presentation, or an asynchronous deck, investors track one thing above all else: consistency. They notice when the quarterly update matches the voice of the pitchbook. They notice when the portfolio overview feels synchronized across platforms. They notice when each presentation seems to pick up the narrative where the last one left off.

On the other hand, when materials look or sound different every quarter — different fonts, different structures, different design rules, different tones — investors feel the discontinuity. They wonder whether the team is stretched or whether responsibilities are unclear internally. Consistency doesn’t just make the materials easier to read; it makes the organization feel more intentional.

Narrative coherence over time is one of the strongest trust signals an investment manager can send — especially in a category as cyclical and sentiment-driven as real estate.

6. Where DG Supports the Presentation Layer

For many clients, investor presentations are the single place where capability gaps strain the organization. Teams may not have the bandwidth to prepare for webinars. They may not have design support for producing clean decks in PowerPoint. They may struggle to translate operational detail into investor-friendly narrative. They may need a neutral party to help them decide what to include — and what to leave out.

DG steps into that gap:

refining the story, sharpening the structure, upgrading the visuals, standardizing the design system, preparing templates, supporting scripts or speaking notes, and ensuring the materials feel aligned with the firm’s broader brand and strategy. For many clients, DG becomes the continuity across multiple formats, multiple audiences, and multiple vehicle types.

When the presentation layer is strong, capital formation feels easier — because investors feel continuously oriented, not periodically reintroduced.

Closing Thought

Investor presentations are no longer occasional events. They are recurring opportunities to reinforce confidence, renew clarity, and show investors that the manager is disciplined not just in the way they invest, but in the way they communicate. Whether delivered in a meeting room, over a webinar, or through an advisor-education session, the mechanics differ but the principle is the same:

a good presentation reduces friction and increases trust.

Real estate managers who approach these moments with intentionality — and who treat communication as a year-round discipline — put themselves in a far stronger position when the next phase of capital formation begins.

Emerging managers tend to imagine LPs evaluating them in a formal setting: the meeting room, the pitchbook walkthrough, the diligence call. But in Fund I fundraising, the most consequential judgments often form before any of that happens — and they’re formed through small digital behaviors the GP barely registers. LPs read these signals the way a seasoned casting director reads posture or tone before an actor delivers a single line. It’s not the main evaluation; it’s the pre-screen.

Digital presence is not just a website. It is a trail of micro-signals — LinkedIn profiles, signatures, bios, email tone, file naming conventions, the structure of a data room, the way materials are shared — that collectively tell LPs whether a GP is ready for institutional capital or is still assembling the scaffolding of a real firm. These signals matter because they offer a glimpse into how the GP will behave when the stakes are higher and the details are messier.

Emerging managers underestimate these signals not because they’re careless, but because they simply haven’t been trained to see what LPs see.

1. Digital Identity Is the First Test of Whether a Firm Is “Real”

LPs begin evaluating you the moment they search your name. Before they know the strategy, before they meet the team, before they read the deck, they are forming a simple judgment: Does this firm actually exist in the institutional sense of the word?

New managers sometimes forget that they are asking LPs to take a leap of faith. There is no long track record, no deep bench of partners, no decades-old brand. LPs need signals that you are building an actual firm — not testing the water, not “seeing how Fund I goes,” but constructing something that will exist in year five and year ten.

Digital presence becomes the earliest proof-of-intent.

If the signals are faint or inconsistent, LPs assume the intent is faint or inconsistent too.

2. LPs Notice Whether the Firm Has Claimed Its Digital Territory

Something as simple as:

- an unclaimed Google Business listing,

- LinkedIn profiles with placeholder language,

- outdated bios,

- or inconsistent job titles

causes LPs to pause — not because they’re judging the brand, but because they’re assessing the organizing competence behind the brand.

Institutional allocators view a digital footprint the way a botanist views root structure. They assume what’s visible is an indicator of what’s invisible. If the visible infrastructure is thin or chaotic, they infer the same about everything else.

3. Tone Is a Digital Behavior, and LPs Hear It Clearly

Tone is one of the most subtle digital cues, and one of the most consequential. LPs pick up emotional data from:

- the firmness or softness of your language

- how you describe your category

- whether your voice sounds confident or apologetic

- whether your tone is stable across mediums

- how your emails read — composed? hurried? overly promotional? underthought?

Tone inconsistencies cause LPs to ask whether the GP has fully formed their worldview. If the voice on the website doesn’t match the voice in the deck — or the voice in the deck doesn’t match the voice in the email — LPs notice instantly. They may not know what’s wrong, but they can feel the mismatch.

For emerging managers, tone is the first “vibe check,” and LPs trust their instincts.

4. Digital Organization Reveals Operational Discipline

LPs are forever trying to separate signal from noise. They know every GP can say the right things. What they’re looking for are signs of how the GP actually works — how they handle process, structure, detail, and follow-through.

Digital organization becomes a proxy:

- a clean, well-labeled data room

- logically named files

- a deck that feels intentionally sequenced

- bios that share a common tone

- a website that reinforces, rather than contradicts, the pitch

These are not compliance checks. They are cognitive shortcuts. LPs assume that a GP who cannot create digital order may struggle to create operational order. And while the correlation isn’t perfect, it’s reliable enough that LPs have learned to trust it.

5. LPs Experience Consistency as Maturity

One of the most underrated digital signals is consistency — not great design, not prolific content, not SEO dominance, but simple, calm consistency across all touchpoints. Even a modest digital presence, when coherent, signals that the GP is ready for institutional conversation.

Emerging managers underestimate how rare digital consistency is. They imagine LPs comparing them to Blackstone or Carlyle. LPs aren’t doing that. They’re comparing them to the dozens of emerging managers who present different versions of themselves across their materials.

Inconsistency reads as drift.

Consistency reads as maturity.

And in Fund I fundraising, maturity is scarce enough to be a differentiator.

6. Content Behaves Like a Digital Signature, Not a Marketing Tactic

Emerging managers often ask whether they “need” content. LPs are not looking for volume. They are looking for evidence that the GP has a point of view — an internal logic strong enough to produce even one or two pieces of thoughtful writing or video.

A small amount of meaningful content signals:

- the GP understands their category,

- they have something to say about it,

- they are confident enough to put those ideas into the world,

- and they intend to be part of the category’s intellectual future.

Content is a way of saying, “We’re not experimenting; we’re committing.”

And in the coming LLM-driven world — where allocators will increasingly ask intelligent systems for recommendations in niche categories — content becomes not just a credibility asset, but a discoverability asset.

Closing Thought

Digital behavior is not decoration. It is the earliest expression of how a GP thinks and how a firm operates. LPs are constantly scanning for signs of maturity, coherence, and intention, and they make these judgments long before the first meeting. Emerging managers who treat digital presence as part of their strategy — not an afterthought to it — close the legitimacy gap faster and create more chances for serendipity.

Fundraising isn’t just about the pitch. It’s about the pre-pitch.

And in that world, digital behavior often speaks first.

Real estate reporting occupies an unusual place in the investment communications landscape. In many structures — non-traded REITs, interval funds, 1031/721 platforms, and certain private vehicles — the legally required reporting is extensive, structured, and tightly governed. Audited statements, compliance-driven updates, NAV disclosures, distribution notices, and required quarterly or annual filings create a baseline rhythm that every manager must follow.

Because of this, managers often assume that “reporting” is largely a compliance exercise. The logic is understandable: if the law already dictates much of what investors must receive, then the communication burden is largely solved. But in practice, the legal layer is only the foundation. The reporting that actually shapes investor confidence—and differentiates one manager from another — lives above the required disclosures.

Investors don’t just want information; they want comprehension. They want clarity, rhythm, and narrative coherence. They want to understand how to interpret what they’re seeing. And they want to feel that the manager is communicating with intention rather than simply meeting an obligation.

This is where reporting becomes a brand advantage rather than a regulatory task.

1. Compliance Reporting Is the Floor, Not the Ceiling

Required filings — financial statements, mandated disclosures, NAV updates, distribution notices — are essential, but they are not designed to help investors understand the story. They are meant to be complete, accurate, and compliant. They are not meant to be persuasive or intuitive.

An institutional LP may be accustomed to deciphering complex statements. A family office CIO may have the pattern recognition to contextualize the numbers quickly. But advisors, RIAs, and high-net-worth investors often need interpretation, not just data. They want to know what the data means in the context of the strategy, the cycle, and the manager’s decisions.

When that layer is missing, reporting feels mechanical and opaque — even if the underlying performance is strong.

The difference between a manager who “checks the box” and one who builds trust is often found in the communication that accompanies the required filings.

2. Investors Respond to Reporting That Explains, Not Just Informs

Real estate is tangible, but real estate reporting often isn’t. Investors receive numbers, tables, and property-level information that doesn’t always translate cleanly into investor-level insight.

What investors want, regardless of sophistication, is orientation:

- What’s happening?

- Why is it happening?

- How should I interpret this?

- Where is the manager focused?

- What’s coming next?

Strong reporting bridges the gap between operational detail and investor comprehension. A quarterly letter or supplemental update doesn’t need to be long. In fact, brevity and clarity are usually more persuasive. But it does need to frame the numbers in a way that helps investors understand the arc of the strategy.

This interpretive layer is where reporting becomes a strategic communication tool rather than a compliance exercise.

3. Consistency Builds More Trust Than Volume

Investors across all channels — institutions, family offices, advisors, RIAs, and individuals — respond strongly to rhythm. When communication appears predictably, with a consistent structure and voice, investors stop wondering whether something is wrong. They begin to experience the manager as steady, attentive, and organized.

Inconsistent reporting, on the other hand, creates unnecessary shadows. Investors don’t assume disaster, but they do assume disorganization. They wonder whether the manager is understaffed, distracted, or stretched. They begin to question whether the team is too thin to manage both investments and investor relations.

Consistency is not about sending more. It’s about creating an expectation and meeting it.

A quarterly letter should feel like part of a series.

A supplemental update should feel like an extension of the brand.

New acquisition or disposition notes should feel like they come from the same organization that produced the pitchbook.

This coherence has a compounding effect. When the next capital formation moment arrives, investors already trust the manager’s communication discipline.

4. Reporting Quality Is a Direct Reflection of the Manager’s Brand

Managers sometimes think of reporting as an operational necessity rather than a brand expression. But for most investors, especially those outside the institutional core, reporting is the primary way they “experience” the firm.

If the pitchbook or website sets the initial impression, reporting sustains it. It reinforces the firm’s identity and signals whether the manager is still aligned with the story that first attracted the investor. Clean, modern, well-organized updates signal a level of attentiveness that carries through to the portfolio.

Conversely, poor reporting — dated formatting, inconsistent charts, overly dense paragraphs, mismatched visuals — suggests something deeper. Investors subconsciously link communication quality to operational discipline. If the materials feel sloppy, they wonder what else might be sloppy. That reaction isn’t always fair, but it is predictable.

Reporting is one of the most powerful brand builders a real estate manager has. Most don’t treat it that way.

5. Different Investors Need Different Levels of Interpretation

One of the challenges (and opportunities) in real estate reporting is the diversity of investor audiences. Institutions, family offices, RIAs, and individuals interpret the same information differently.

Institutions tend to be analytical and process-driven. They want clarity but can handle detail. Family offices vary widely — some are highly sophisticated, others more instinctual — but all tend to appreciate directness. Advisors and RIAs need materials that are digestible enough to pass along to clients. High-net-worth individuals interpret information more emotionally, often responding more to the story than the mechanics.

A well-constructed reporting package can speak to all four groups without diluting its message. The key is making the structure intuitive: clear headlines, concise narratives, well-organized exhibits, and a steady voice.

Everyone reads for clarity. Few have patience for clutter.

6. Where DG Adds the Most Value

Most real estate teams are not built to produce institutional-quality reporting in-house — and they shouldn’t be. Their core expertise is investing, not communication. Reporting becomes a bottleneck because it requires writing, design, narrative judgment, and production discipline — all skills that tend not to be concentrated on an investment team.

DG’s support solves that bandwidth and capability gap. We help clients:

- modernize their reporting templates;

- translate operational detail into investor-accessible language;

- ensure that recurring documents match the brand and the website;

- produce clean charts and exhibits that don’t feel repurposed or mismatched;

- maintain consistency across quarters and across vehicles;

- create reporting that feels like an extension of the pitchbook (not a separate universe).

And — perhaps most importantly — we help managers communicate proactively during cycle shifts, market volatility, or periods of operational complexity.

Reporting does not have to be ornate. It has to be clear, coherent, and consistently executed. That alone separates a manager from the pack.

Closing Thought

Required filings satisfy the rules.

Thoughtful reporting satisfies the investors.

The managers who build trust over the long term understand the difference. They know that reporting is not just informational—it’s interpretive. It’s the way investors experience the discipline, maturity, and attentiveness of the platform.

Real estate managers who treat reporting as a brand-strengthening activity — not just a compliance obligation — find that future capital conversations begin on much firmer ground. Communication doesn’t raise capital by itself, but it builds the confidence that makes capital formation easier.